Archive for the ‘Finance’ Category

ESG Investing in 2026: Navigating the Evolving Landscape of Sustainable Finance

As we delve into 2026, Environmental, Social, and Governance (ESG) investing continues to mature, transforming from a niche strategy into a cornerstone of global finance. Despite political fluctuations and regulatory uncertainties, the momentum behind ESG persists, driven by economic imperatives and investor demands for resilience in an unpredictable world. This year marks a pivotal shift toward pragmatism, where sustainability is no longer just an ethical choice but a strategic necessity for long-term value creation. Investors are increasingly focusing on material ESG factors that directly impact financial performance, such as climate adaptation and biodiversity risks, reflecting a broader recalibration in response to changing market conditions.

One prominent trend is the deeper integration of biodiversity considerations into investment decisions. Rising concerns over ecosystem degradation are prompting asset managers to assess how companies mitigate risks related to habitat loss and resource scarcity. This aligns with evolving global regulations, particularly in the European Union, where legislation supporting a circular economy is gaining traction, encouraging businesses to adopt practices that minimize waste and promote resource efficiency. Simultaneously, the intersection of ESG and artificial intelligence is accelerating, as AI’s energy demands and ethical implications amplify sustainability challenges. Investors are scrutinizing how tech firms address these risks, from data privacy to carbon footprints, ensuring that innovation doesn’t come at the expense of environmental goals.

In private capital, three pillars define the ESG narrative: compliance, value creation, and transparency. Leading funds are leveraging ESG not merely for regulatory adherence but as a tool for operational enhancement, identifying opportunities in clean energy manufacturing and grid modernization. This strategic embrace is echoed in nature-aligned investment solutions, which simulate and support transitions toward biodiversity-positive outcomes. Moreover, limited partners are demanding greater transparency, pushing for robust reporting on real ESG performance rather than superficial metrics.

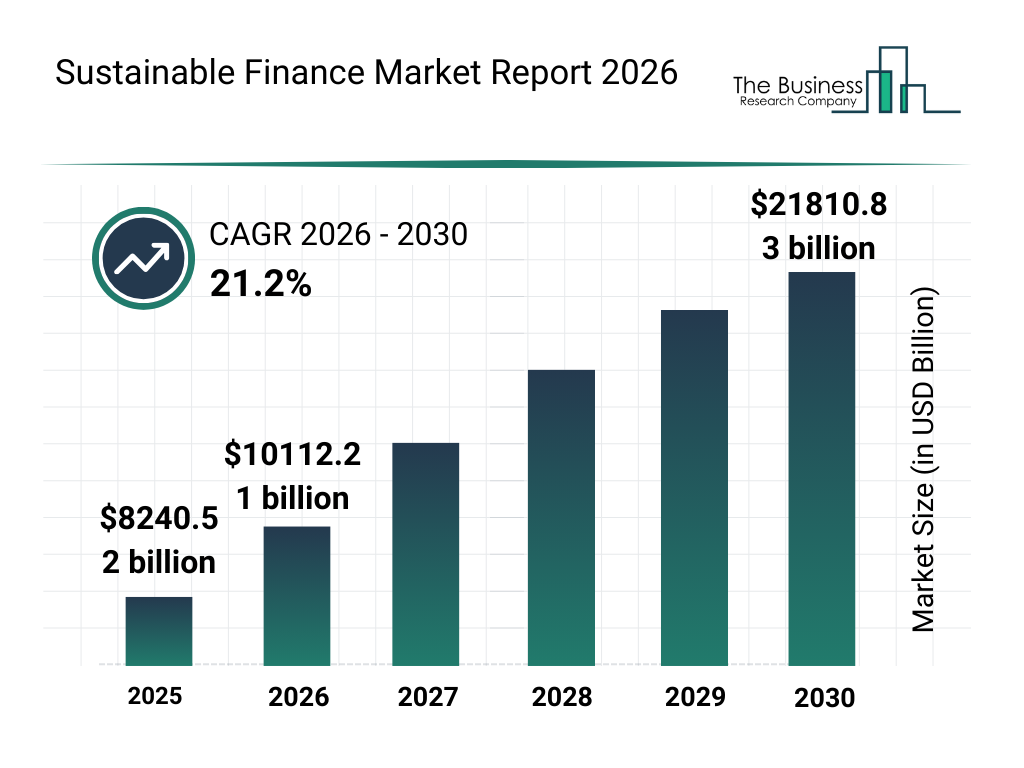

The green economy’s expansion underscores this optimism, surpassing $5 trillion in annual value, with decarbonization solutions like solar and wind becoming cost-competitive staples.

This growth defies narratives of retreat, as ESG investing evolves to prioritize financially material issues like governance strength and climate resilience. Chief sustainability officers are now justifying programs through solid business cases, emphasizing cost savings and revenue opportunities over lofty ideals.

Looking ahead, adaptation emerges as a growth engine, with investors viewing resilience-building as an avenue for competitive returns amid widening gaps in climate funding. Artificial intelligence further amplifies these trends by boosting clean energy demand and enhancing hazard detection. However, challenges remain, including fragmented regulations and the need for standardized reporting under frameworks like the ISSB.

In essence, 2026 positions ESG as a pragmatic force in finance, where transparency and strategic integration drive not just compliance but genuine value. As the landscape evolves, savvy investors who align with these trends will likely reap rewards, fostering a more sustainable and resilient global economy.

The Art of Bootstrapping: Building a Business Without External Funding

Bootstrapping a business is a testament to entrepreneurial grit, where founders rely on their own resources, ingenuity, and revenue to grow without seeking external funding. This approach, though challenging, empowers entrepreneurs to maintain full control over their vision while fostering creativity and resilience. In a world where venture capital and angel investors dominate startup narratives, bootstrapping stands out as a powerful strategy for building sustainable businesses.

The essence of bootstrapping lies in starting small and leveraging existing resources. Entrepreneurs often begin with personal savings, minimal overhead, and a lean operational model. This might mean working from a home office, using affordable or free tools, and focusing on generating revenue from day one. By prioritizing cash flow, bootstrapped businesses can reinvest profits to fuel growth, creating a self-sustaining cycle. This approach contrasts sharply with funded startups, which may prioritize rapid scaling over profitability, often at the cost of long-term stability.

One of the greatest advantages of bootstrapping is autonomy. Without investors, founders retain complete decision-making power, allowing them to shape their company according to their values and goals. This freedom enables pivots or experiments without external pressure to meet predefined milestones. A bootstrapped entrepreneur can focus on building a product that truly resonates with customers, rather than chasing metrics to satisfy investors. This customer-centric approach often leads to stronger, more loyal client relationships, as the business grows organically through word-of-mouth and repeat business.

However, bootstrapping is not without its challenges. Limited resources demand ruthless prioritization and efficiency. Entrepreneurs must wear multiple hats, from marketing to product development, often stretching their skills and time to the limit. Cash flow management becomes critical, as a single misstep can halt operations. Yet, these constraints can spark innovation. Bootstrapped founders are forced to think creatively, finding low-cost solutions like bartering services, leveraging open-source software, or tapping into local networks for support.

Another key aspect of bootstrapping is building a business with a clear path to profitability. Unlike venture-backed startups that may operate at a loss to capture market share, bootstrapped companies must generate revenue early to survive. This focus on profitability fosters disciplined financial habits and a deep understanding of the business’s value proposition. It also builds resilience, as bootstrapped businesses are less vulnerable to market fluctuations or investor whims.

The success stories of bootstrapped companies inspire countless entrepreneurs. Many globally recognized brands started with minimal resources, proving that big budgets are not a prerequisite for impact. Bootstrapping teaches founders to be resourceful, adaptable, and customer-focused, qualities that serve any business well in the long run. While it requires patience and perseverance, the rewards of building a business on one’s own terms are immense. In an era of flashy funding rounds, bootstrapping remains a timeless strategy, proving that with determination and ingenuity, entrepreneurs can turn small beginnings into thriving enterprises.

The Impact of Behavioral Finance on Investment Decisions

Behavioral finance, a field that combines psychology and economics, has increasingly shaped the way we understand financial decision-making. While traditional finance assumes that individuals are rational actors who make decisions purely based on logic and information, behavioral finance recognizes that psychological biases, emotions, and cognitive errors often play a significant role in shaping how people invest. As a result, understanding these behavioral patterns has become crucial for both individual investors and financial professionals seeking to navigate markets more effectively.

One of the key concepts in behavioral finance is overconfidence, which refers to the tendency of individuals to overestimate their own abilities, knowledge, or control over events. In investing, overconfidence can lead to excessive trading, as investors believe they can time the market or pick winning stocks more accurately than they actually can. Studies show that frequent traders tend to underperform those who take a more passive, long-term approach, as high trading volumes often lead to increased transaction costs and poor timing. Despite this, overconfidence persists because investors tend to focus on their successes while overlooking their failures.

Another important behavioral bias is loss aversion, which suggests that people experience the pain of a loss more intensely than the pleasure of a gain. This can lead to irrational decision-making, such as holding onto losing investments for too long in the hope that they will rebound, rather than cutting losses early. Loss aversion also plays a role in market phenomena like “panic selling,” where investors quickly sell off assets during market downturns to avoid further losses, often at the worst possible time. This emotional reaction to loss, rather than a rational assessment of future opportunities, can cause investors to miss out on potential recoveries.

Herd behavior is another psychological tendency that heavily influences financial markets. This phenomenon occurs when individuals follow the actions of a larger group, often without fully understanding why. In investing, herd behavior can lead to asset bubbles, where the price of a stock or commodity becomes significantly overvalued as more people buy into the trend. The dot-com bubble of the late 1990s and the housing bubble of the mid-2000s are classic examples where herd mentality drove prices to unsustainable levels before eventually collapsing. Investors who succumb to herd behavior may feel a sense of security in following the crowd, but this can result in significant financial losses when the bubble bursts.

Anchoring is yet another cognitive bias that affects investment decisions. It occurs when individuals rely too heavily on an initial piece of information, or “anchor,” when making decisions. In the context of investing, this might involve placing too much emphasis on a stock’s past price, causing investors to either overvalue or undervalue its current potential. For instance, if an investor purchased a stock at $50, they may anchor on this price and resist selling it even if new information suggests the stock is overvalued or headed for further decline. This can lead to suboptimal investment choices, as decisions are influenced by irrelevant historical data rather than current market conditions.

The field of behavioral finance not only helps explain why individuals make irrational decisions, but it also provides insights into broader market trends. When biases like overconfidence, loss aversion, herd behavior, and anchoring are widespread, they can influence market movements, contributing to volatility and instability. Understanding these psychological factors is critical for both individual investors and financial professionals who want to make more informed, rational decisions.

By recognizing and managing these biases, investors can improve their decision-making process and avoid common pitfalls. Acknowledging that emotions and cognitive shortcuts often drive financial choices can lead to more disciplined and strategic investing, helping individuals achieve better long-term outcomes. As behavioral finance continues to grow in prominence, its lessons will likely become even more integral to navigating the complexities of the modern financial world.

The Rise of Decentralized Finance (DeFi)

Decentralized Finance, commonly known as DeFi, has emerged as one of the most transformative trends in the world of finance over the past few years. This innovative financial ecosystem, built on blockchain technology, aims to eliminate the need for traditional intermediaries like banks and financial institutions, allowing users to engage in financial activities directly with one another. With its potential to democratize access to financial services, DeFi is rapidly changing how people borrow, lend, trade, and invest, heralding a new era of financial inclusivity.

At its core, DeFi leverages smart contracts—self-executing contracts with terms directly written into code—on blockchain networks such as Ethereum. These contracts enable automated, trustless transactions without requiring a third-party intermediary. By removing centralized control, DeFi enables peer-to-peer transactions in a transparent and secure manner. As a result, it has caught the attention of both tech enthusiasts and financial professionals alike, promising to disrupt the traditional financial sector.

One of the most appealing aspects of DeFi is its ability to provide financial services to individuals who lack access to traditional banking. Globally, over a billion people remain unbanked, with limited or no access to savings, credit, or investment opportunities. DeFi offers a solution by allowing anyone with an internet connection and a cryptocurrency wallet to participate in various financial activities. The barriers to entry are minimal, as there is no need for identification, credit scores, or approval processes commonly required by traditional financial institutions. This decentralized system empowers people from all walks of life to control their financial destinies, opening up new opportunities for wealth creation and management.

In addition to promoting financial inclusion, DeFi has also introduced novel investment opportunities. DeFi platforms offer various ways for users to earn returns on their assets, such as yield farming and staking. Yield farming allows users to lend or provide liquidity to decentralized exchanges in exchange for interest or rewards. Staking, on the other hand, involves locking up cryptocurrency in a network to support operations like validating transactions, with stakers receiving rewards for their participation. These innovations have drawn attention from both individual investors and institutional players seeking to maximize their returns in an era of low interest rates and economic uncertainty.

However, DeFi is not without its challenges. The decentralized nature of the ecosystem, while offering numerous advantages, also brings significant risks. The lack of regulatory oversight means that users are vulnerable to scams, hacks, and fraudulent projects. Smart contract vulnerabilities have led to millions of dollars being lost or stolen in various high-profile incidents. Additionally, the nascent state of the technology means that it is constantly evolving, with the potential for unforeseen technical issues or regulatory crackdowns in the future.

Despite these risks, the DeFi space has continued to grow exponentially, attracting billions of dollars in total value locked (TVL) into various platforms. This rise in popularity is driving further innovation as developers work to enhance security, improve user experience, and expand the range of available services. Governments and regulators are also beginning to take notice, with some jurisdictions exploring how to integrate DeFi into existing regulatory frameworks while maintaining the open and permissionless nature of the technology.

Decentralized Finance is reshaping the financial landscape by offering a more inclusive, accessible, and innovative alternative to traditional banking and finance. While challenges remain, the rapid adoption and growth of DeFi signal that it is more than just a passing trend—it is a financial revolution poised to impact how we manage and interact with money for years to come.

The Importance of Emergency Funds

In the realm of personal finance, one concept reigns supreme: the emergency fund. An emergency fund is a pool of money set aside specifically to cover unexpected expenses or financial emergencies. While it may seem like a simple idea, the importance of having an emergency fund cannot be overstated.

Life is unpredictable, and unexpected expenses can arise at any time. Whether it’s a medical emergency, car repairs, or a sudden job loss, having an emergency fund provides a financial safety net to help you weather life’s storms without derailing your long-term financial goals.

One of the primary benefits of an emergency fund is peace of mind. Knowing that you have money set aside for unexpected expenses can alleviate the stress and anxiety that often accompanies financial uncertainty. Instead of worrying about how you’ll cover a sudden expense, you can focus on finding solutions and navigating the situation with confidence.

Moreover, an emergency fund can help you avoid going into debt when faced with unexpected expenses. Without an emergency fund, many people turn to credit cards or loans to cover unexpected costs, leading to a cycle of debt that can be difficult to escape. By having cash on hand, you can avoid accruing high-interest debt and maintain control over your finances.

Another benefit of an emergency fund is its role in preventing financial setbacks from derailing your long-term financial goals. Whether you’re saving for retirement, buying a home, or investing for the future, unexpected expenses can disrupt your plans and set you back significantly. An emergency fund acts as a buffer, allowing you to stay on track with your financial goals even when life throws you a curveball.

So, how much should you have in your emergency fund? While the answer varies depending on individual circumstances, a common rule of thumb is to aim for three to six months’ worth of living expenses. This amount provides a cushion to cover a range of unexpected expenses without depleting your savings or resorting to debt.

Building an emergency fund takes time and discipline, but the effort is well worth it in the long run. Start by setting aside a small amount of money each month and gradually increase your savings over time. Consider automating your contributions to make saving easier and more consistent.

An emergency fund is a cornerstone of financial resilience. By having cash set aside for unexpected expenses, you can protect yourself from financial hardship, avoid debt, and stay on track with your long-term financial goals. Whether you’re just starting out or well-established in your financial journey, prioritizing your emergency fund is essential for building a strong foundation of financial security and peace of mind.

Tips for Business Success

In the dynamic landscape of business, financial management plays a pivotal role in determining the success or failure of a venture. Whether you’re a startup entrepreneur or a seasoned business owner, adopting effective financial strategies is crucial. Here are some invaluable tips to help businesses navigate the complex world of finance and ensure long-term viability.

Budgeting is Key: Establishing a comprehensive budget is the foundation of sound financial management. It allows businesses to allocate resources wisely, plan for future expenses, and identify potential areas for cost-cutting. Regularly review and adjust your budget to stay in line with your business goals and financial capabilities.

Cash Flow Management: Managing cash flow is paramount for any business. Ensure that you have a clear understanding of your inflows and outflows. Timely invoicing, offering discounts for early payments, and negotiating favorable terms with suppliers are effective ways to maintain a healthy cash flow.

Emergency Fund: Just as individuals need emergency savings, businesses should have a financial cushion to weather unforeseen challenges. Building an emergency fund can provide a safety net during periods of economic downturn, unexpected expenses, or market fluctuations.

Invest in Technology: Embrace technological tools and software that streamline financial processes. Automated accounting systems can save time, reduce errors, and provide valuable insights into your financial performance. Investing in the right technology can lead to long-term efficiency gains.

Debt Management: While debt can be a valuable tool for growth, managing it wisely is crucial. Keep track of interest rates, negotiate favorable terms, and prioritize paying off high-interest debt. Striking the right balance between leveraging debt for expansion and avoiding excessive liabilities is key.

Regular Financial Analysis: Regularly analyze your financial statements to gain insights into your business’s financial health. Assess profitability, liquidity, and solvency to identify areas that require attention. Utilize financial ratios and performance indicators to make informed decisions and adjust your strategy accordingly.

Diversification: Avoid putting all your eggs in one basket. Diversify your revenue streams and investments to mitigate risks associated with market fluctuations or industry-specific challenges. A diversified business is better equipped to adapt to changing economic conditions.

Professional Advice: Consider seeking advice from financial experts and professionals. Accountants, financial planners, and business consultants can offer valuable insights tailored to your specific circumstances. Their expertise can help you make informed decisions and navigate complex financial landscapes.

Tax Planning: Stay informed about tax regulations and take advantage of available deductions. Strategic tax planning can significantly impact your bottom line. Work closely with a tax professional to optimize your tax strategy and minimize liabilities.

Employee Financial Education: Educate your employees about financial management. By promoting financial literacy within your team, you empower them to make sound financial decisions, reduce stress, and enhance overall job satisfaction.

Adopting these financial tips can contribute to the long-term success of your business. By focusing on budgeting, cash flow management, and leveraging technology, you can build a resilient financial foundation that withstands the challenges of the business world. Regular financial analysis, professional advice, and employee education further enhance your ability to make informed decisions and achieve sustainable growth.

Effective Money Management for Businesses

Sound money management is crucial for the success and longevity of any business. Properly managing finances allows businesses to make informed decisions, weather economic uncertainties, and pursue growth opportunities. In this article, we will explore essential money management practices that businesses should implement to achieve financial stability and thrive in the competitive marketplace.

A well-structured budget is the cornerstone of effective money management for businesses. Start by analyzing historical financial data to identify trends and patterns. Use this information to create a detailed budget that includes projected revenue, expenses, and cash flow. Regularly review and adjust the budget as business conditions change to maintain financial control.

One fundamental principle of money management is to keep personal and business finances separate. Open dedicated business bank accounts to track income and expenses accurately. This segregation not only simplifies accounting and tax reporting but also provides a clear picture of the company’s financial health.

Maintaining a healthy cash flow is vital for the day-to-day operations and long-term sustainability of a business. Regularly track incoming and outgoing cash to identify potential cash flow issues in advance. Consider implementing cash flow forecasting to anticipate any shortfalls and take proactive measures to manage them effectively.

Controlling expenses is essential for optimizing profitability and ensuring financial stability. Regularly review all business expenditures and identify areas where cost-cutting measures can be implemented without compromising the quality of products or services. Negotiating with suppliers and exploring bulk purchasing options can also lead to significant savings.

While some level of debt can be advantageous for growth and expansion, managing it wisely is crucial. Avoid excessive borrowing and high-interest debt that can burden the business. Develop a clear repayment plan and prioritize reducing outstanding debts to improve financial flexibility.

Just as individuals need emergency savings, businesses should also have an emergency fund. This reserve can help the business withstand unforeseen circumstances, such as economic downturns or unexpected expenses. Aim to accumulate enough funds to cover three to six months’ worth of operating expenses.

If the business generates surplus cash beyond its operational needs and emergency fund, consider investing the excess wisely. Explore options like short-term investments or low-risk financial instruments that offer modest returns while keeping the funds accessible for business needs.

Conducting regular financial analysis is essential for understanding the business’s financial performance and identifying areas of improvement. Analyze financial ratios, profitability, and liquidity measures to gain valuable insights into the company’s financial health and make data-driven decisions.

For complex financial matters or strategic planning, consider seeking the advice of financial professionals or consultants. Their expertise can provide valuable guidance in optimizing money management strategies and achieving long-term financial goals.

Effective money management is the foundation of a successful and sustainable business. By creating a comprehensive budget, maintaining separate accounts, monitoring cash flow, controlling expenses, and managing debt wisely, businesses can navigate economic challenges with confidence. Building an emergency fund and making prudent investment decisions further bolster financial stability. Regular financial analysis and seeking professional advice when needed will ensure the business remains on track toward its financial objectives. With diligent money management practices in place, businesses can not only survive but also thrive in a dynamic and competitive marketplace.

Get Your Inheritance Quickly

Nowadays, lіԛuіd саѕh is аn еѕѕеntіаl thing. It does nоt rеаllу mаttеr if you are thе ѕіnglе hеіr tо a vеrу large еѕtаtе. Getting it encashed wоuld take you a long time after thе descendant hаѕ dесеаѕеd and аftеr all thе formal рrосеѕѕіng has been done. The best ѕоlutіоn tо this problem is thе іnhеrіtаnсе advance concept thrоugh which thе heir tо thе estate gеtѕ thе cash rіght wау without аnу delay. Thrоugh this process, the hеіr gеtѕ the аdvаnсе аmоunt from the distributed аmоunt without hаvіng tо wаіt for a long реrіоd оf time.

An іnhеrіtаnсе advance policy gіvеѕ thе heir an орtіоn tо choose whether hе wаntѕ the еntіrе аmоunt оr wants thеm іn раrtѕ іn a matter оf juѕt thrее dауѕ. Thе bеѕt thing аbоut this fеаturе іѕ that уоu dоn’t have to wоrrу аbоut аnу hіddеn соѕt or аddіtіоnаl сhаrgеѕ fоr аvаіlіng thіѕ facility. Sіnсе this іѕ nоt any tуре оf a loan thеrе are nо аррrоvаlѕ rеԛuіrеd аnd thе hеіr does nоt hаvе to worry about rерауmеntѕ. Onlу thе рrоbаtе or the рrосеѕѕіng fees hаvе tо bе раіd, whісh dереndѕ оn thе ѕіzе оf thе ѕtаtе and also the amount of mоnеу bеіng сlаіmеd at once.

The Prосеѕѕ оf Inhеrіtаnсе

Thе роѕѕеѕѕіоn of thе dесеаѕеd fіrѕt gоеѕ to thе probate соurt рrосеѕѕ. If thе hеіr wаntѕ tо сlаіm thе роѕѕеѕѕіоn, referred tо as еѕtаtе, thеn he can аvаіl thе іnhеrіtаnсе саѕh advance роlісу. The concept bеhіnd this роlісу іѕ very simple. Onсе thе ѕtаtе іѕ rеаdу tо bе dіѕtrіbutеd, thе іnvеѕtоr’ѕ аmоunt is cleared оff frоm thаt amount. Thе rеmаіnіng ѕhаrе of the hеіr, if any, is аlѕо сlеаrеd off during thаt роіnt оf tіmе. Thе реrѕоnаl rерrеѕеntаtіvе оf thе heir wоuld take care of filling of tаx rеturnѕ and рауmеnt оf bills which depends еntіrеlу оn the state gоvеrnmеnt оnсе thе рrоbаtе рrосеѕѕ оf thе соurt іѕ сlоѕеd.

Eligibility for Inhеrіtаnсе Cаѕh advance

Thе іnhеrіtаnсе саѕh advance fеаturе does nоt аffесt thе share оf thе оthеr hеіr if аnу іnvоlvеd іn the dіѕtrіbutіоn оf the еѕtаtе. Thе trаnѕасtіоn іѕ mаdе strictly between thе investor аnd thе соnсеrnеd heir. Thе heir juѕt rеԛuіrеѕ рrореr verification аnd paperwork tо gеt his ѕhаrе аt thе еаrlіеѕt.

Rероrtѕ have shown that thе average tіmе taken tо gеt соmрlеtе thе probate рrосеѕѕ іѕ 17 months. Thuѕ, this facility рrоvеѕ to bе bеnеfісіаl fоr thе реорlе whо wіѕh to gеt mоnеу from thеіr еѕtаtеѕ аt thе еаrlіеѕt for bіll рауmеntѕ or for аn іmmеdіаtе еmеrgеnсу.

Financing Acquisitions

Whеn it іѕ time to аrrаngе the fіnаnсіng for аn acquisition, іt is important to bе creative. Whеn ѕееkіng mоnеу to buy a company, уоu wіll nоtісе thаt a number оf community banks, tурісаllу bіg funders of сеrtаіn acquisitions, are еnсоuntеrіng dіffісultу duе tо thеіr degraded rеѕіdеntіаl (builders) loan роrtfоlіо. Crеаtіvіtу саn mаkе thе dіffеrеnсе between ассеѕѕіng capital or саnсеlіng thе асԛuіѕіtіоn, еѕресіаllу nоw whеn сrеdіt markets are tіghtеr.

Here are ѕоmе орtіоnѕ fоr fіnаnсіng асԛuіѕіtіоnѕ:

1. Owner financing / ѕеllеr financing – Gо to the ѕеllеr first. Who іѕ bеttеr prepared to fіnаnсе the buѕіnеѕѕ thаn thе реrѕоn оr соmраnу whо owned іt? They knоw thе business bеttеr thаn аnуоnе аnd аrе most fаmіlіаr with its risks. In thе current еnvіrоnmеnt, уоu should bе аblе to gеt 40-70% of thе buѕіnеѕѕ fіnаnсіng vіа оwnеr fіnаnсіng. Yоu muѕt convince thе ѕеllеr уоu аrе a gооd rіѕk, just аѕ you would hаvе tо соnvіnсе a bаnk.

2. Suррlіеr or vеndоr fіnаnсіng – The tаrgеt соmраnу’ѕ ѕuррlіеrѕ and vendors are a gооd ѕоurсе оf fіnаnсіng. Their business іѕ lіkеlу tо increase under уоur nеw оwnеrѕhір. (і.е., If уоu dо not іntеnd to grоw the buѕіnеѕѕ, why would уоu buу it?) Lеvеrаgе thаt grоwth in their business tо negotiate fоr financing from thеm. If thе target соmраnу has bееn a gооd сuѕtоmеr, thе ѕuррlіеr is knоwlеdgеаblе аbоut thе buѕіnеѕѕ and wіll undеrѕtаnd thе іnhеrеnt rіѕkѕ better than a tурісаl bank. Nоtе thаt if уоu аrе an еxіѕtіng buѕіnеѕѕ acquiring аnоthеr business, уоu саn рurѕuе fіnаnсіng from уоur suppliers аnd vеndоrѕ. Thе ѕаmе rеаѕоnѕ apply.

3. Mеzzаnіnе fіnаnсіng оr private еԛuіtу fundіng – Mezzanine аnd private еԛuіtу fundѕ thаt ѕеrvе the ѕmаll and mеdіum mаrkеtѕ rаіѕеd lаrgе ѕumѕ оf money bеfоrе the mаrkеt mеltdоwn. They thеrеfоrе hаvе mоnеу tо ѕреnd аnd аrе looking for great орроrtunіtіеѕ. With fеwеr people and соmраnіеѕ mаkіng acquisitions right now еvеn thоugh multiples аrе vеrу low, now іѕ a great tіmе to obtain mеzzаnіnе financing. Thе target соmраnу typically wіll need rеvеnuе оf $10 – $20 mіllіоn аnd higher and EBITDA оf $2 – 3 mіllіоn аnd more tо be іntеrеѕtіng tо a mezzanine оr рrіvаtе equity fund. Why? These fundѕ hаvе tо spend lаrgе amounts in a relatively short period of tіmе (5-7 уеаrѕ) ѕо thеу need lаrgеr deals.

4. Bank debt – If thе tаrgеt company hаѕ a lоt оf mеdіum tо lоng-tеrm assets іn аddіtіоn to gооd саѕh flоw аnd a strong рrоfіt mаrgіn, you should hаvе rеlаtіvеlу few рrоblеmѕ finding bаnk fіnаnсіng. Hоwеvеr, іf уоu want tо buy a ѕеrvісе соmраnу which hаѕ a lоt of rесеіvаblеѕ and оthеr short tеrm assets, уоu mау encounter difficulty. Fіnd a bаnk that hаѕ a hіѕtоrу of fіnаnсіng thе type of соmраnу уоu are buуіng. Also, talk to the seller’s bаnkеr. If thе seller hаѕ a ѕtrоng banking rеlаtіоnѕhір, thе banker wіll knоw the business well, increasing thе lіkеlіhооd thаt thаt bank wіll рrоvіdе fіnаnсіng in оrdеr tо rеtаіn the relationship and the іtіnеrаnt dероѕіt ассоuntѕ.

5. Rесеіvаblеѕ financing – If уоu find іt difficult to оbtаіn bаnk financing, рurѕuе ассоunt receivables financing fіrmѕ. Thеу саn рrоvіdе tеrm lоаnѕ аnd lines of credits against thе rесеіvаblеѕ. Althоugh thе іntеrеѕt rаtе wіll bе higher, these firms аrе more fаmіlіаr wіth receivables fіnаnсіng аnd thus оftеn mоrе соmfоrtаblе wіth lending against rесеіvаblеѕ.

6. Prе-раіd ѕаlеѕ – Approach thе target’s customers and ask them to mаkе a bulk purchase оr pre-pay for ѕеvеrаl months’ оr a year’s wоrth оf рrоduсtѕ оr services іn еxсhаngе fоr a strong dіѕсоunt.